Vikalp Thukral. Quantitative researcher working at the intersection of derivatives, stochastic modeling, and real‑time market data.

I'm a recent Master of Financial Engineering graduate from UCLA Anderson (Dec 2025), now building agentic‑AI quant research tooling and interactive analytics — including a live, browser‑rendered implied volatility surface for any US‑listed equity, an institutional‑grade risk dashboard, and a real‑time commodities analytics terminal.

Builder first,

researcher always.

I came to quantitative finance through an unusual door — six years of large‑scale data and product engineering at American Express, where I owned the Enterprise Data Warehouse and rebuilt legacy PySpark pipelines that cut overnight runtimes from 24 hours to under four. That foundation in systems and scale shaped how I think about models: they only matter if they're fast, reproducible, and usable by someone other than the author.

At UCLA Anderson MFE I focused on the rigorous side of that equation — stochastic calculus, derivatives pricing, computational methods, and econometrics — and I'm now a Quant Research Analyst at UCLA Anderson, developing Python‑based quant research tooling and risk analytics modules with agentic AI (Claude Code) to accelerate calibration and backtesting of derivative pricing models. I'm also running systematic alpha research on the WorldQuant BRAIN platform. In 2025 my team placed Top 4 of 30 in the IAQF International Student Competition, modelling bubble dynamics with GARCH‑DCC and LPPLS.

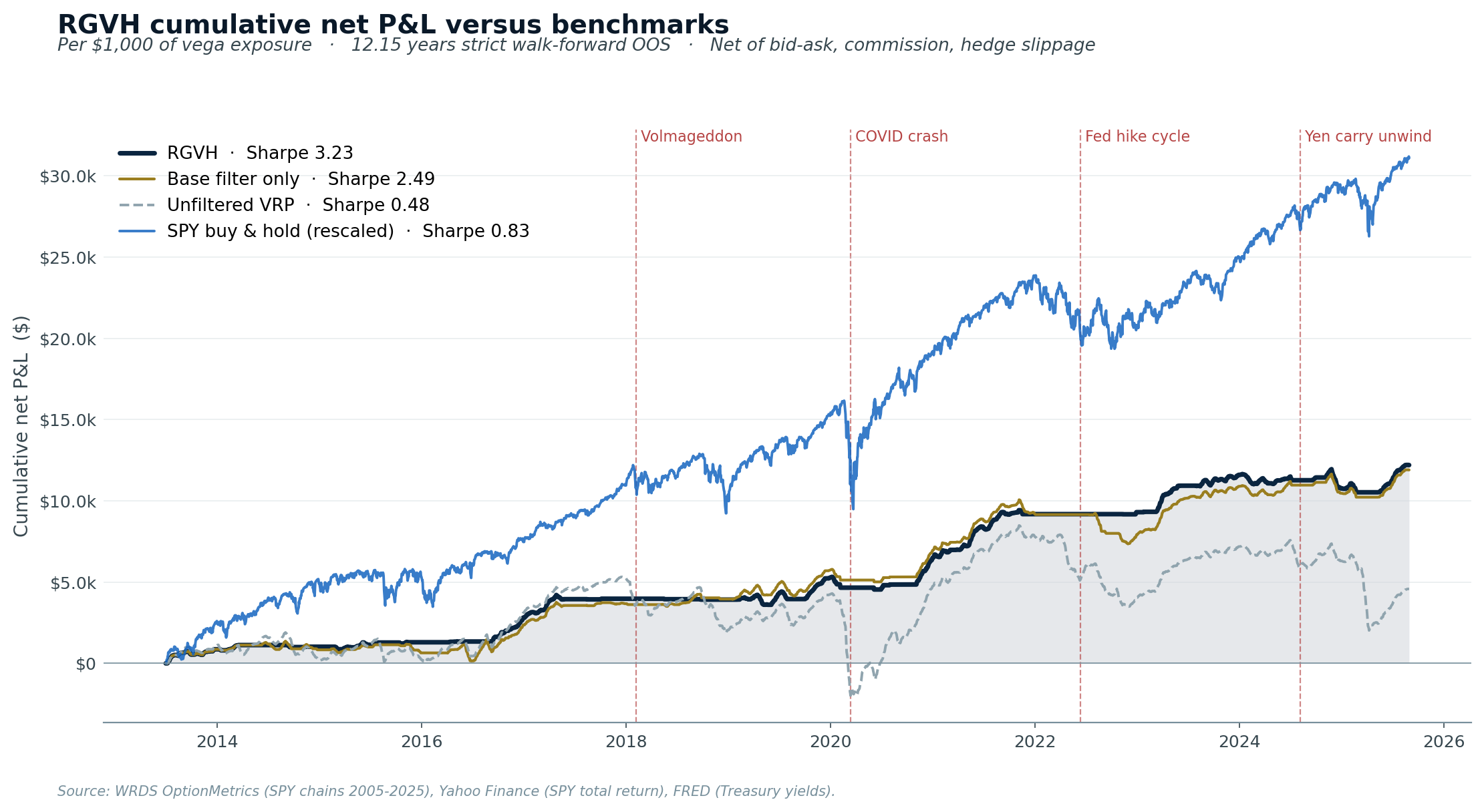

Outside of coursework I ship things: an in‑house options pricing library (binomial, trinomial, Crank‑Nicolson PDE solvers, variance‑reduced Monte Carlo), a Fama‑French five‑factor replication suite, a cash‑flow waterfall engine for securitized loans, and a live 3D volatility surface you can visit below. I care about the craft of making quantitative research legible.

Volatility Surface

An interactive 3D implied‑volatility surface visualizer for any US‑listed equity. Pulls live options chains from Yahoo Finance through a custom FastAPI backend, cleans the chain, and renders a smoothed Plotly mesh with four Z‑axis metrics, camera presets, and side‑by‑side term‑structure and skew‑slice mini‑charts.

Risk Dashboard

Real‑time portfolio risk monitoring with interactive VaR/CVaR gauges, GARCH‑based volatility forecasting, factor exposure decomposition, and configurable stress‑test scenarios.

Commodities Dashboard

Real‑time commodity futures analytics with term structure curves, volatility analysis, seasonality, correlation matrices, and spread analysis across crude oil, gold, natural gas, and more.

Research, pricing,

and market modelling.

View all projects →

Geeks for Greeks — Bubble Dynamics

GARCH‑DCC volatility modelling and LPPLS critical‑time bubble detection across multi‑asset regimes. Read the competition paper.

Read Paper ↗Risk Analytics Dashboard

Real‑time portfolio risk dashboard with VaR/CVaR gauges, GARCH forecasting, factor exposure decomposition, and stress‑test scenario analysis.

View Dashboard ↗Commodities Dashboard

Real‑time commodity futures analytics with term structure, volatility models, seasonality, correlation matrices, and interactive charting.

Launch App ↗Volatility Surface Explorer

Real‑time 3D implied vol surface with 10 color palettes, four Z‑metrics, smoothing, and side‑by‑side term structure & skew slice charts.

Launch App ↗

Six years across data, product, and research.

Quant Research Analyst

Developing Python‑based quant research tooling and risk analytics modules in support of faculty research, leveraging agentic AI (Claude Code) to accelerate prototyping, calibration, and backtesting of derivative pricing and risk models across asset classes. Conducting systematic alpha research on the WorldQuant BRAIN platform.

Associate — Quantitative Risk Analytics

Enhanced liquidity risk and portfolio monitoring tools with Python and automated SQL workflows, strengthening day‑to‑day risk infrastructure for the credit portfolio. Built Tableau dashboards translating exposure, concentration, and policy‑adherence metrics into actionable views for senior management.

Associate — Data & Product Management

Product owner for the Enterprise Data Warehouse; spearheaded ingestion and production updates for 1B+ rows of customer financial data. Refactored legacy PySpark/HIVE jobs from 24h → 3‑4h runtimes.

Associate — Data Analytics

Root‑cause analysis and rapid production resolution for data‑quality issues in Agile Scrum teams. Built Excel/VBA and Tableau dashboards for enterprise data health.

Let's talk

about markets.

Actively and selectively exploring full‑time quantitative research and trading roles. Always happy to chat about derivatives pricing, volatility modelling, or anything that lives at the edge of code and markets.